Payment orchestration is taking the e-commerce industry by storm. But as with any new technology that disrupts how things have always been, come mixed feelings and reception. Payment orchestration is no different. Even though many e-commerce businesses have received this new technology with open arms, some are still hesitant to adopt it due to its potential risks and challenges. However, the benefits of payment orchestration far outweigh the risks.

This article will break down what payment orchestration is by presenting the benefits and limitations of this technology so that, as a merchant, you can make an informed decision on how to select and implement the right solutions.

What is Payment Orchestration?

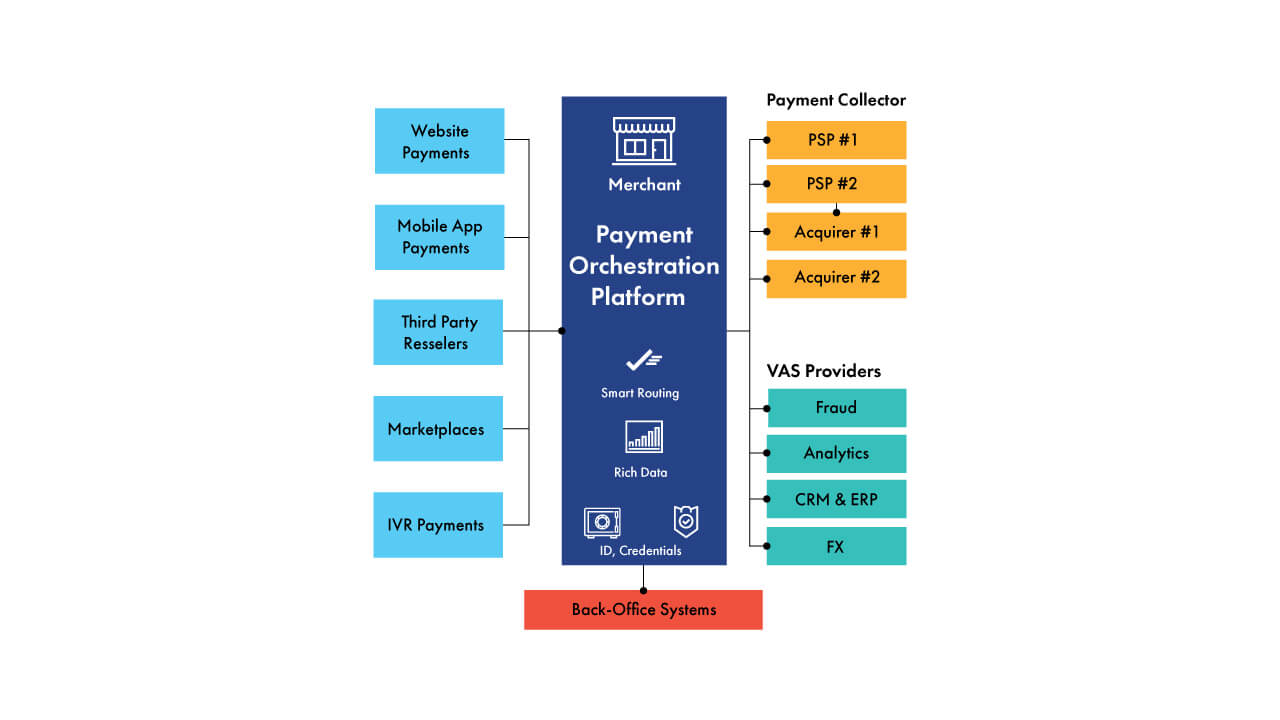

Payment orchestration is a fintech solution that helps e-commerce businesses automate and streamline payment processing to ensure the most efficient route for a transaction. It integrates different payment methods and gateways into a single platform, which allows businesses to accept payments from various sources, such as credit cards, debit cards, e-wallets, and bank transfers. Ultimately, this simplifies the process for both the merchant and the customer, allowing e-commerce companies to save on multiple integrations while delivering a seamless checkout process for customers.

This fintech solution leverages a payments orchestration layer (POL), a software platform that enables businesses to manage all aspects of their payment processing, including authorization, clearing, and settlement. By providing a single platform, you can manage all your payment service providers (PSPs). POLs help to reduce PSP adoption time while optimizing transactions and following a dynamic decision-making approach.

How Do Payment Orchestrators Work?

Understanding how payment orchestrators fit into digital payments processing is essential to leveraging their full capabilities and benefits. In a nutshell, payment orchestrators reduce the number of false failed payments and increase conversion rates for e-commerce platforms while reducing transaction costs by finding the optimal transaction route. Here is a detailed process of how payment orchestrators work when integrated into an e-commerce payment platform:

- On the checkout page, the customer chooses their preferred payment method. Then a payment orchestrator provides secure input fields or UI components to collect payment data.

- Once the payment data is collected, the orchestrator's smart routing feature analyzes the transaction details, including payment method, currency, location, and other factors, to determine the optimal payment service provider or acquirer.

- The payment orchestrator forwards the transaction request to the selected payment service provider or acquirer. The provider performs necessary authorization checks, such as verifying the availability of funds or performing fraud checks. The request is propagated to the acquiring bank. The payment response is then sent back to the e-commerce platform through the orchestrator.

The acquiring bank then communicates whether the issuing bank has authorized the payment by sending a message back to the payment gateway and you (the merchant).

Benefits of Payment Orchestrators

As mentioned earlier, payment orchestrators provide various benefits for e-commerce merchants. These include:

Reduced payment failures

Failed transactions can have a substantial impact on conversion rates and revenue. According to Visa and Mastercard analysis, one in five payments is lost through 3D secure (3DS). While a big chunk of failed payments are customer-related issues, such as insufficient funds, incomplete card data, etc., there are often failed transactions due to technical problems and a lack of backups or options in the payment processing infrastructure. Implementing a payment processing platform, such as a payment orchestrator, can minimize these failures through smart routing.

Geographical flexibility

While local PSPs can reduce payment costs, these PSPs may only be available in some countries. Unfortunately, this can also be true of payment gateways, PSPs, and acquirers who claim to be ‘global.’ This can end up limiting your customers to only certain geographical areas and, thus, reducing your revenues.

With payment orchestration platforms, you can integrate various payment providers from across the globe at affordable rates and terms. Dynamic payment routing helps e-commerce merchants better control payment flows by switching providers in case of issues with the PSP, their availability in the region, authorization or approval rates, etc.

Access to multiple payment methods

Suppose your e-commerce business has customers with different payment preferences, such as mobile wallets or buy now, pay later (BNPL). In that case, you can easily add these methods to your website without the challenge of integrations. Moreover, many payment orchestrator platforms offer online retailers access to pre-approved PSPs, eliminating the need for lengthy approval processes.

Limitations of Payment Orchestrators

As payment orchestration platforms are a relatively new approach, current implementations of POL are limited, and there are some potential limitations that you should expect with payment orchestrators, including:

Complex payment flows

Payment orchestration enables routing payment requests through different payment gateways based on factors like availability, rates, and geography. However, it does not inherently offer the capability to dynamically modify the payment flow, encompassing the entire payment journey from initiation to approval. This includes situations when authorization occurs at an unusual time (e.g., order dispatching), when support is needed for dual-message payments, when limitations are in place for the number of captures exceeding the authorized amount, and when the ability to process partial refunds is needed.

The payment flow requirements of a business may evolve, such as during peak sale seasons or leading up to holidays. However, integrating an orchestrator into non-standard payloads, where authorization does not occur at checkout, can present challenges. Orchestrators may not support such scenarios, making accommodating unique payment flows that deviate from the standard process difficult.

Difficulty meeting multiple providers’ requirements

While having access to multiple PSPs is a plus, managing all their different requirements can also be a problem. For instance, when using the payment interfaces, certain PSPs will charge a fee (either monthly or yearly) that is not dependent on how much you use it. These fees are also accrued even when no transactions are made. Even though it is technically possible with payment orchestrators, you must remember that it might lead to some additional expenses. You still will have to pay for the integration with the orchestrator and the integration with each provider. Even if you do not use the integration, you still pay because of contractual obligations.

Regulation challenges

Regulations can also present several challenges in the implementation of payment orchestration platforms. For instance, the EU's regulations on online payments, such as Strong Customer Authentication (SCA) and PSD2, can interfere with the process of payment orchestration. This is because these rules require online merchants to secure online payments throughout the payment process. With this, e-commerce platforms may require their EU customers to complete multiple checks, lengthening the checkout process.

This can be off-putting for many customers who prefer a swift process and may affect sales and revenues. And even though these platforms can use third-party 3DS service providers, which adds an extra level of payment protection, the payment gateway may not accept or want to work with them. That is why it is important to remember that POL provides the basic functionality of payment gateways and rarely supports PSP-specific features, and it can be challenging to integrate third-party solutions with orchestrators even if PSP supports it out of the box.

Other Key Challenges:

- The choice of settlement accounts can pose challenges when it comes to payment orchestration. If it is not possible to add multiple bank accounts, there may be limitations in deciding where funds should be transferred. For instance, different regions may require separate accounts. This issue is particularly relevant for marketplaces or software platforms that do not natively support connected accounts or the ability to accept payments on behalf of other businesses. Moreover, payment orchestrators typically do not facilitate payment routing between businesses, customers, and recipients who need to receive payments.

- Dynamic routing prevents customers from selecting and paying via payment methods with limited routing options. This includes payment methods selected payment orchestrators may not support, such as MOTO transactions, cash-based vouchers, or bank redirects. With dynamic routing, the payment orchestration system ensures customers are directed to appropriate payment methods based on availability and compatibility.

- One of the difficulties associated with payment orchestration platforms is their general inability to carry out network tokenization, introduced by VISA, Mastercard, and AMEX, that allows cards to be tokenized at the root level instead of relying on third-party vaults. This innovation reduces the need for payment orchestration in cases requiring failover mechanisms or card vaulting. With network tokenization, the card schemes control the generation and management of card tokens, streamlining the payment process and reducing dependencies on external orchestration systems.

Conclusion

Payment orchestration is a game-changing technology in the e-commerce industry, offering numerous benefits for merchants. However, there are still some limitations. It is, therefore, important that you understand the strengths and limitations of payment orchestration to make informed decisions and maximize the benefits of this technology.

Key Takeaways

- Payment orchestrators integrate multiple payment methods and gateways into a single platform, simplifying the checkout process for both merchants and customers.

- The benefits of payment orchestrators include reduced payment failures, geographical flexibility, and access to multiple payment methods.

- The limitations of payment orchestrators include complex payment flows, difficulty managing multiple providers' requirements, regulation challenges, and overdependence on third-party services.

Despite the limitations, payment orchestrators have many advantages, and merchants can make informed decisions to leverage this technology and improve their payment processing efficiency. Are you ready to leverage the power of payment orchestrators and revolutionize your payment processing? At DataArt, we have over 20 years of experience and deep expertise in payments. Our highly trained engineers, backed by industry sector knowledge and ongoing technology research, can help you navigate the complexities of payment orchestrators and unlock their full potential for your business. Contact us today, and let's explore how we can create custom payment solutions that improve your operations and open new markets.